Mortgage rates have been unpredictable lately, which can make planning a home purchase feel tricky. While you can’t control the market, there are steps you can take to secure the best possible rate—and it all starts with being informed.

Why Mortgage Rates Fluctuate

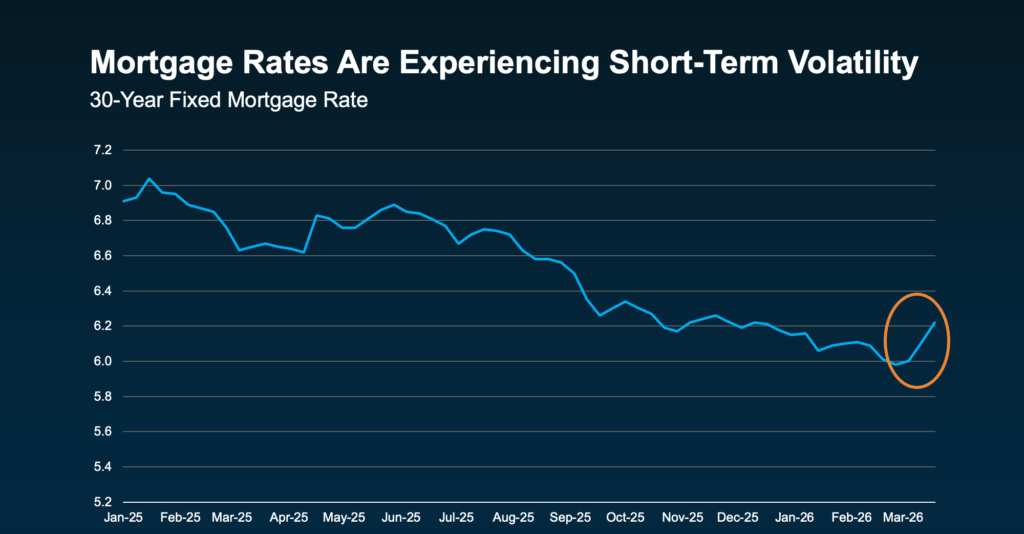

Recent data from Freddie Mac highlights this volatility. After more than a year of declining rates, we’ve recently seen an uptick.

Rate fluctuations like this are normal. Even within the past year, rates have risen and fallen several times. Economic uncertainty and global events often trigger these swings. As Investopedia notes:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets … mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

Trying to time the market is risky—rates can move in ways no one can predict.

Focus on What You Can Control

1. Your Credit Score

Your credit score heavily influences the rate you qualify for. Even modest improvements can reduce your monthly payment. Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

Check your score regularly and work with a trusted loan officer if you need guidance on improving it.

2. Your Loan Type

Different mortgage types—conventional, FHA, USDA, VA—come with distinct eligibility rules, benefits, and rates. According to the CFPB:

“Rates can be significantly different depending on what loan type you choose.”

Exploring your options with one or more lenders can help you find the best fit.

3. Your Loan Term

The length of your mortgage—15, 20, or 30 years—affects your interest rate, monthly payment, and total interest paid. Freddie Mac advises:

“Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Work with a lender to select the term that aligns with your budget and long-term goals.

Bottom Line

If you’re thinking about buying a home now, accept that you can’t control where rates go next.

What you can do is focus on what matters: your credit, your loan type, and your loan term. By working with a trusted lender and controlling the controllables, you can position yourself to get the best rate possible.

Ready to make your move? Let’s focus on what you can control—and make it happen.