Renting can feel cheaper and simpler than owning a home—especially in today’s market. No repair bills, no property taxes, no worrying about interest rates. You just pay your rent and move on.

But here’s what often gets overlooked: renting doesn’t help you build long-term financial security. Homeownership does. Simply by owning a home, you’re growing your net worth year after year.

If you’ve been questioning whether buying still makes financial sense, the long-term numbers tell a very clear story.

Renting vs. Owning: The True Cost Difference

One major distinction between renting and buying is where your money goes. When you rent, your monthly payment benefits your landlord—and once it’s paid, it’s gone for good. When you buy, part of your monthly mortgage payment comes back to you in the form of equity. That’s wealth created as your home appreciates in value and as you pay down your loan.

So while renting may look more affordable upfront, it comes with a hidden long-term cost: you’re not building any financial foundation. And that cost is bigger than many people expect.

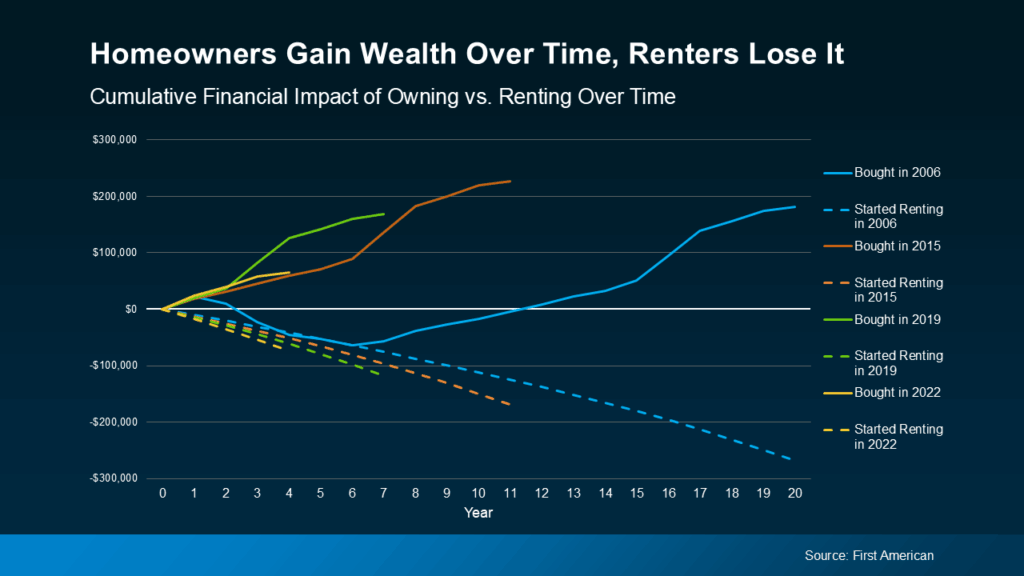

First American recently compared the long-term financial outcomes of renting versus owning. They evaluated mortgage payments, taxes, insurance, upkeep, and repairs against how much equity builds through rising home values and mortgage paydown. They ran this analysis across several key market periods:

- 2006: Start of the housing bubble

- 2015: Ten years ago

- 2019: Pre-pandemic, a more normal market

- 2022: When mortgage rates spiked

Across every period, the results were the same: renters lost money over time, and homeowners gained it.

A recent chart shows the pattern clearly. The solid lines—representing homeowners—show steady growth in wealth the longer they stay in their homes. The dashed line—representing renters—shows consistent money spent with no financial gain.

Time spent owning builds wealth. Time spent renting doesn’t.

Even after including property taxes, insurance, and maintenance, homeowners still came out ahead in every scenario. Renters, on the other hand, spent thousands without gaining any long-term return.

This doesn’t mean buying is always cheaper right away. But the longer you own, the bigger the wealth gap becomes.

Affordability Is Slowly Improving

You may still feel like buying a home just isn’t realistic right now—and that’s understandable.

The past few years have been challenging for buyers. But conditions are beginning to shift. Mortgage rates have eased, home prices are stabilizing, and incomes are rising. And according to Zillow, typical monthly payments are now slightly more affordable than they were at this time last year. Not dramatically, but enough to matter.

Buying a home isn’t suddenly effortless. But it is becoming more attainable than it was just a few months ago. And history clearly shows: in the long run, owning a home remains one of the most reliable ways to build wealth.