Renting often feels like the simpler option at first. You don’t need a large down payment, you’re not responsible for unexpected repairs, and there’s no long-term commitment tying you down.

But over time, rent increases can start to add up. When your rent keeps going up year after year, the flexibility that once felt appealing can begin to feel expensive—especially when you realize you’re not building any equity. That’s when many renters start to feel stuck in the cycle.

There’s also a lot of discussion today about how buying a home isn’t affordable anymore. However, when you look closely at the numbers, the situation may be more favorable than many people expect, particularly given recent market changes.

Buying Can Be More Affordable Than Renting in Many Areas

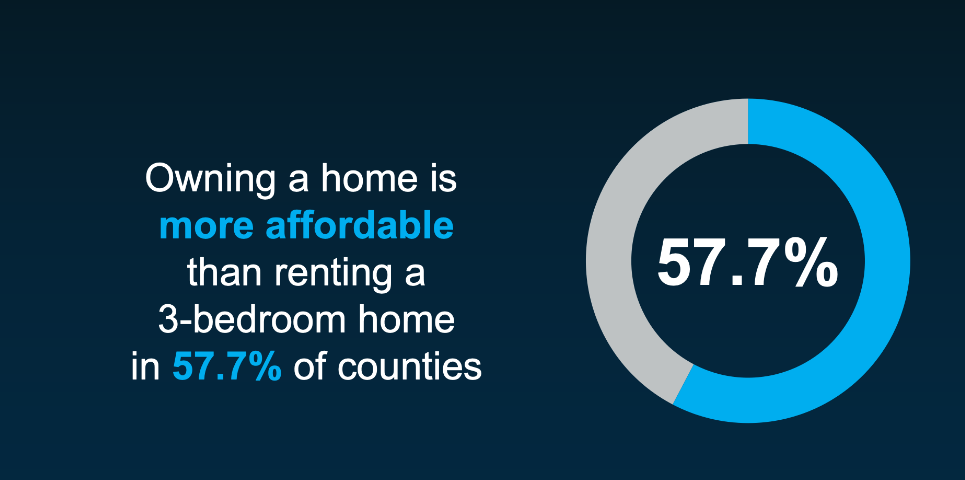

In many markets today, the monthly cost of owning a home can actually be lower than renting a three-bedroom property. Recent data from ATTOM shows that this is the case in nearly 58% of counties across the United States.

This comparison already factors in common ownership costs such as insurance and typical maintenance expenses.

In other words, even though purchasing a home might initially seem like the more expensive choice, the data suggests that rent often places a greater strain on monthly budgets than homeownership. Slower home price growth, increased housing inventory, and gradually easing mortgage rates are all contributing to more manageable monthly mortgage payments.

Affordability Still Depends on Location

While the overall national trend is shifting, buying isn’t more affordable than renting in every market or for every renter.

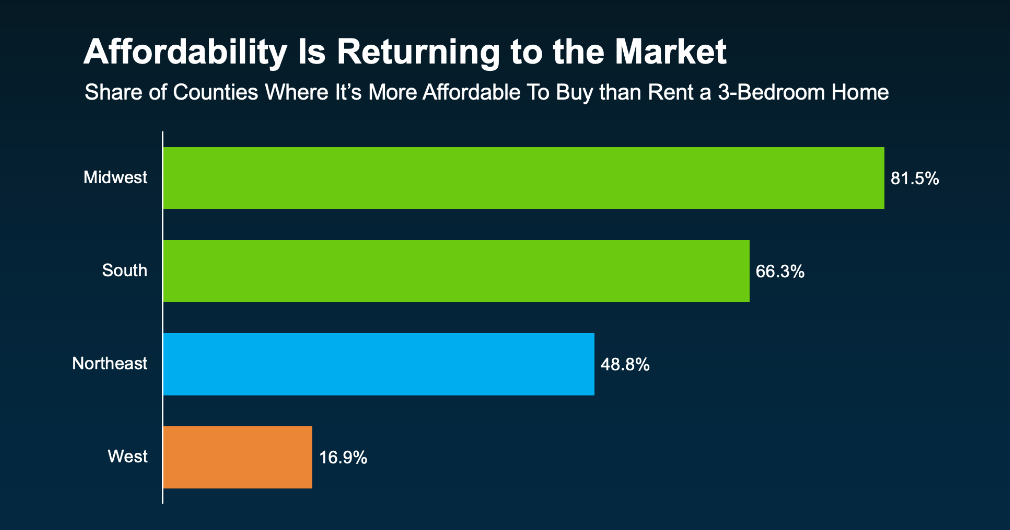

Although owning is more affordable than renting in nearly 58% of U.S. counties, the percentage varies significantly by region.

The most noticeable improvements are happening in the Midwest and the South, while in many areas of the Western U.S., affordability can still feel challenging.

The key takeaway is that housing affordability is highly local. The best way to understand your options is to evaluate the numbers in your specific market.

What’s Still Holding Many Buyers Back?

You might agree with the points above but still feel concerned about the upfront costs of buying a home. That’s a common concern among renters.

For many people, the biggest obstacle isn’t just the monthly mortgage payment—it’s coming up with the down payment.

However, many buyers don’t realize how much support may be available. Across the country, thousands of down payment assistance programs exist, and many qualified buyers aren’t aware they’re eligible.

On average, these programs can provide around $18,000 in assistance.

This kind of financial support can help cover part of your down payment or closing costs, potentially reducing the amount you need to save before purchasing a home.

When combined with improving affordability—thanks to easing mortgage rates and stabilizing home prices—homeownership may be more achievable than it first appears.

Bottom Line

This doesn’t mean everyone should rush out and buy a home tomorrow.

But it does highlight an important point: renting isn’t always the most affordable option people assume it is. In many cases, buying may be more realistic than it seems once you look at the full picture.

If you’re currently renting and feel like homeownership is something for “someday,” it might be worth having a conversation to explore your options and see what could be possible for you.