Foreclosures are on the rise, which might immediately remind you of the 2008 housing crash. Let’s examine that connection and see what the data tells us.

While foreclosure filings have increased, they’re far from reaching crisis levels—and they’re not headed in that direction. Here’s why.

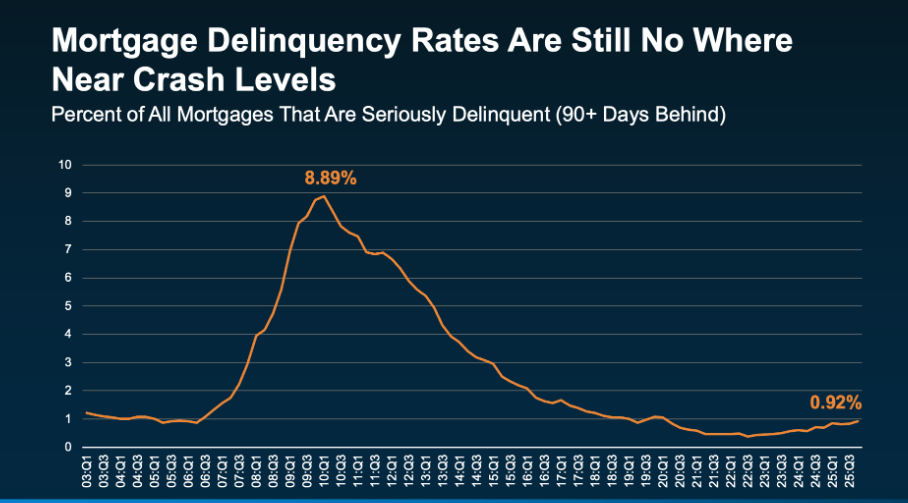

The Role of Serious Delinquencies

Let’s start by looking at serious delinquencies, which are loans where homeowners are over 90 days behind on payments.

Although these delinquencies have seen a slight increase, data from the New York Fed shows they remain relatively low and nowhere near the levels seen during the market crash (refer to the graph below):

Currently, only about 1% of mortgages are seriously delinquent—just 1 in 100. During the crash, that number was closer to 9%, or 1 in 11. That’s a significant difference.

It’s also important to note that not all delinquencies lead to foreclosure filings. Many homeowners who fall behind on payments negotiate repayment plans with their lenders, as banks also want to avoid a wave of foreclosures.

Foreclosures Are Even Lower Than Delinquencies

Foreclosure filings are even rarer than delinquencies. According to ATTOM, just 0.3% of all homes are currently in foreclosure. Moreover, not all of those will result in a completed foreclosure. In other words, it’s more of a ripple than a wave.

Why Aren’t There More Foreclosures If People Are Falling Behind?

You might wonder why we’re not seeing more foreclosures, despite some people struggling financially. The answer lies in priorities.

When faced with financial pressure, many households prioritize their mortgage payments over other debts because losing their home is their biggest concern.

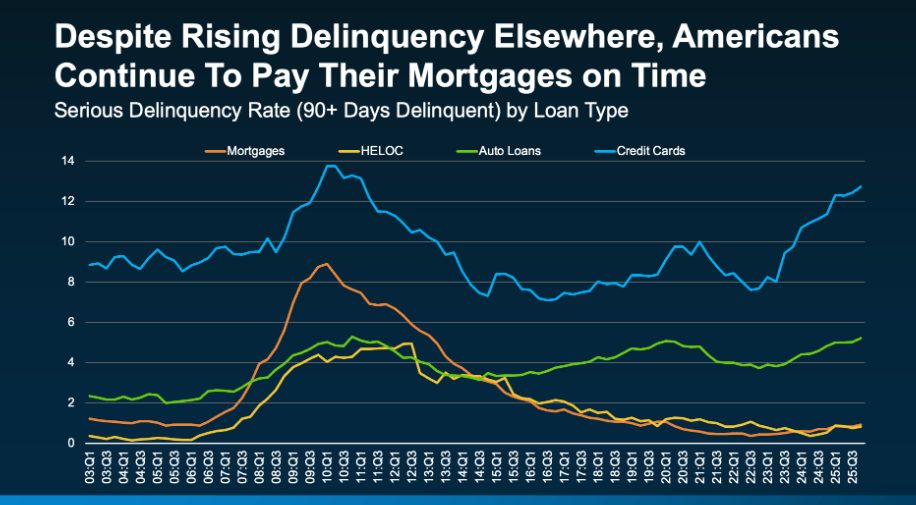

The New York Fed’s data shows an uptick in delinquencies for credit cards and auto loans, but mortgage delinquencies have not surged at the same rate. This suggests that while people may fall behind on other payments, they’re determined to keep their homes, especially when they have substantial equity in them.

Home Equity Makes a Big Difference

Many homeowners have built significant equity over recent years, which gives them more options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… often still have equity in their homes. They have the option to sell and avoid foreclosure, walking away with some of that equity.”

This is a major shift from 2008, when many homeowners owed more than their homes were worth and couldn’t sell. Today, selling is a viable solution for many. Even if equity doesn’t fully cover the mortgage, homeowners are encouraged to work with their loan servicers early on to explore alternatives to foreclosure.

Conclusion

Yes, foreclosure filings are on the rise, but they’re nowhere near the levels seen during the crash. Homeowners today are in a much stronger position with more equity and more options than they were in 2008.

Instead of panicking over the headlines, the key is to keep things in perspective. Based on the data, this situation is not a repeat of 2008.