The lending landscape in California is evolving rapidly in 2026. Lenders who understand local market trends, adapt to regulatory changes, and embrace modern technology can gain a strong competitive edge. This guide highlights key insights, strategies, and opportunities for lenders in today’s market.

Exploring California’s Lending Market

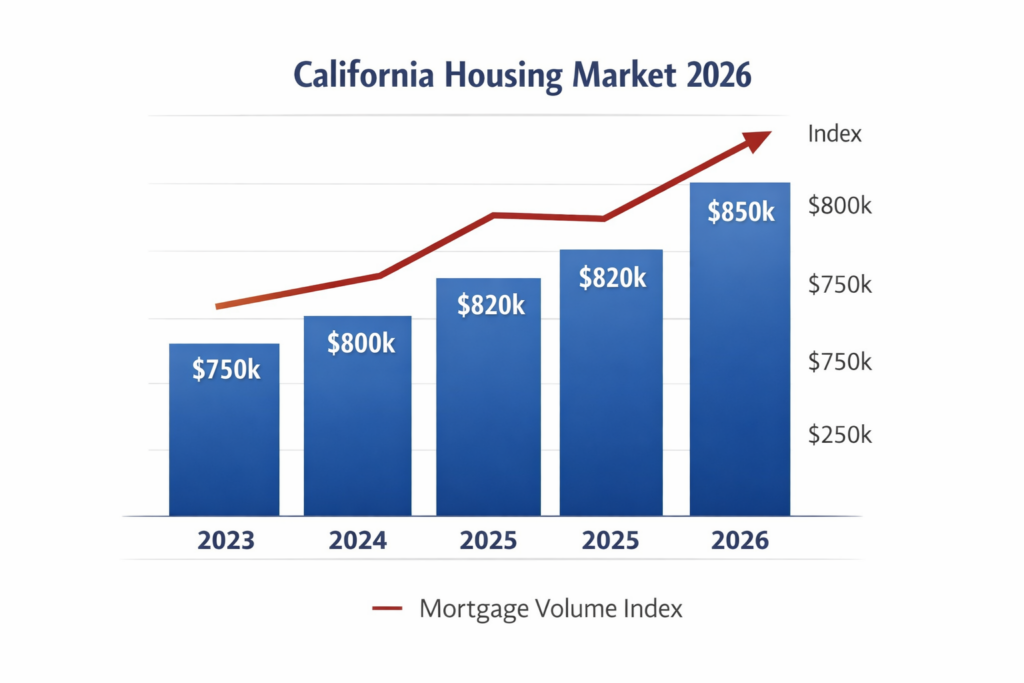

Trends in Residential Lending

- High-demand urban areas like Los Angeles and the Bay Area are seeing rising mortgage volumes and higher average loan sizes.

- Affordability-challenged regions face tighter credit and growing household debt, creating unique market niches.

- Conforming loan limits in high-cost counties have increased in 2026, offering more flexibility for middle-income borrowers.

Key takeaway: Balance growth by targeting both high-value urban markets and emerging suburban areas.

Opportunities in Commercial and Small-Business Lending

- Multifamily and small-business loans are on the rise due to housing shortages and entrepreneurial activity.

- Lenders offering SBA loans or commercial real estate financing gain an edge in underserved markets.

Tip: Partner with local banks or fintechs to expand your reach while managing risk.

Emerging Lending Trends

1. Technology and Process Automation

AI-powered credit decisioning, automated underwriting, and cloud-based loan origination systems are becoming essential.

Automation improves efficiency, reduces errors, and supports compliance.

Actionable insight: Integrate technology that combines risk assessment, borrower verification, and regulatory reporting.

2. Growth in Private Credit and Alternative Lending

Alternative lending is expanding, creating opportunities in niche and mid-market segments.

Non-bank lenders are increasingly competing with traditional banks, positioning private credit as a growth area.

Strategy: Collaborate with alternative lenders and design specialized products for underserved segments.

3. Addressing Climate and Environmental Risks

Properties in wildfire- and flood-prone regions require specialized underwriting.

Proactive climate risk assessment can safeguard portfolios and attract environmentally responsible borrowers.

Navigating Regulatory Requirements

Compliance Landscape

California is strengthening fair lending enforcement beyond federal standards, emphasizing borrower protection.

Environmental and climate-related disclosures are increasingly affecting mortgage approvals.

Best practice: Incorporate compliance measures at every stage of the lending process, from origination to servicing.

Actionable Strategies for Growth

- Enhance Customer Experience: Offer transparent loan options, real-time updates, and position officers as trusted advisors.

- Leverage Technology: Use AI-driven origination systems for faster, more accurate decisions and ensure secure data handling.

- Refine Risk Models: Adapt credit criteria to local trends and consider alternative data for non-traditional borrowers.

- Diversify Product Offerings: Include SBA loans, DSCR, small-business, and investor-focused products, while targeting niche and suburban markets.

Key Opportunities in 2026

- Urban markets continue to drive mortgage demand.

- Suburban and secondary markets are emerging as high-growth areas.

- Technology adoption increases efficiency and compliance readiness.

- Alternative lending and private credit offer new revenue streams.

- Climate-conscious underwriting differentiates lenders and protects portfolios.

Final Thoughts

California’s lending market in 2026 is shaped by innovation, regulations, and economic trends. Lenders who embrace technology, understand local market dynamics, and uphold strong compliance practices are well-positioned for success.

A customer-focused, data-driven approach allows lenders to grow responsibly, reduce risk, and build trust—creating a competitive advantage in a complex market.