If you’ve been wondering whether buying a home is even realistic right now, you’re not alone. With rising property prices and higher mortgage rates, renting often feels like the simpler—or sometimes only—option.

And if renting suits your current situation, that’s perfectly fine.

But when you’re seriously comparing the two, there’s one important factor that often gets missed:

how each choice shapes your future.

What Renting Offers—And What It Doesn’t

Renting comes with clear benefits, especially in today’s market:

- Lower upfront costs

- Fewer responsibilities for maintenance

- Flexibility to move easily

These advantages can make life easier in the short term. However, there’s a tradeoff that many people quietly worry about.

A large number of potential buyers are concerned about the long-term impact of renting—and it mainly comes down to one thing:

Renting doesn’t build future value.

When you pay rent, you’re securing a place to live, but you’re not building ownership or equity. There’s no asset in your name, no long-term return, and no value growing over time.

So while renting provides convenience today, it doesn’t contribute to your financial growth tomorrow.

How Owning a Home Builds Wealth

Homeownership works differently.

Each mortgage payment helps you build equity—the portion of the property you truly own, calculated as the difference between the home’s value and the amount you still owe.

Here’s why that matters:

- Your equity increases with every payment

- Your property may appreciate in value over time

- You’re gradually building wealth while paying for housing

Instead of money leaving your pocket with no return, it’s being invested into something you own.

That’s one reason homeowners typically have a higher net worth than renters. It’s not necessarily about earning more—it’s about consistently building value over time.

Think of it like this:

A home is a savings tool you live in.

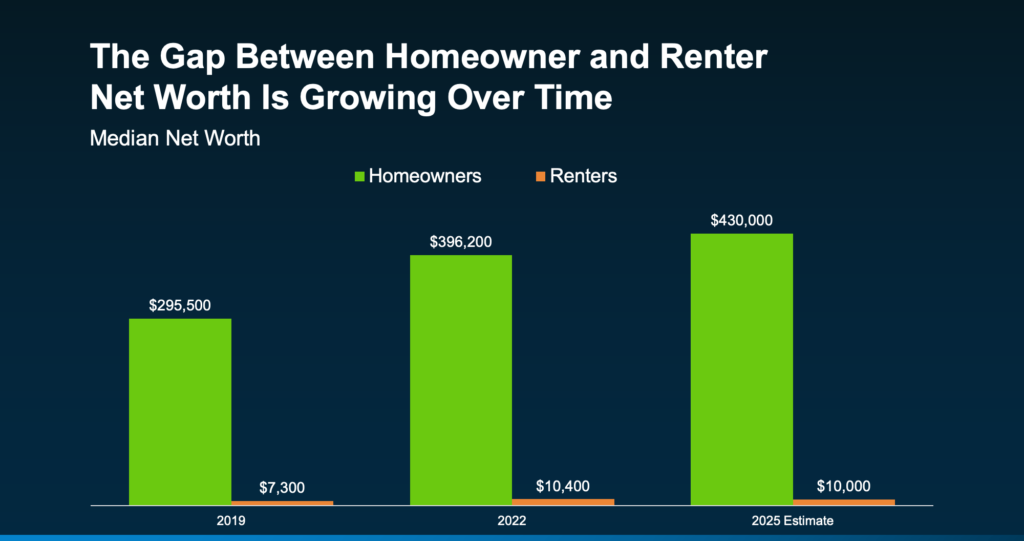

The Growing Wealth Gap

The financial gap between renters and homeowners continues to widen.

Over time, homeowners build wealth through equity and property appreciation, while renters keep making payments without gaining ownership.

Even when property values grow slowly, homeowners are still progressing financially—while renters often remain in the same position.

This brings up a simple but important point:

You’re always paying for a place to live—the question is, whose investment are you supporting?

- Renting contributes to your landlord’s wealth

- Owning contributes to your own

Should You Buy a Home Now?

The honest answer: it depends.

Buying a home is a long-term commitment and only makes sense if:

- You’re financially prepared

- You plan to stay in one place for a while

- It fits comfortably within your budget

If you’re not there yet, renting can absolutely be a smart temporary choice.

But if owning a home is one of your goals, the best step you can take right now is to get clear on your situation.

Speak with a real estate expert, evaluate your finances, and understand what it would take to make the shift. You may be closer than you think—or you’ll at least have a solid plan moving forward.

Either way, you replace uncertainty with clarity.

Bottom Line

Renting might feel easier today, but it can have long-term financial limitations.

If building wealth and stability is your goal, homeownership remains one of the most reliable ways to achieve it.

And it doesn’t begin with buying a house—it starts with understanding your options, creating a plan, and knowing what’s possible for you.